Welcome to our monthly REITView newsletter – where we analyze the latest national trends in real estate investment trusts (REITs) and their implications for investors and the Nevada real estate market. REITs own and often operate a pool of income-producing real estate assets. Investors can purchase a liquid stake in these portfolios – think of them as mutual funds for real estate.

While REITs are not the biggest players in Nevada’s commercial real estate landscape, secondary markets like Las Vegas with above-average population and job growth are likely to attract REITs looking for value and growth opportunities.

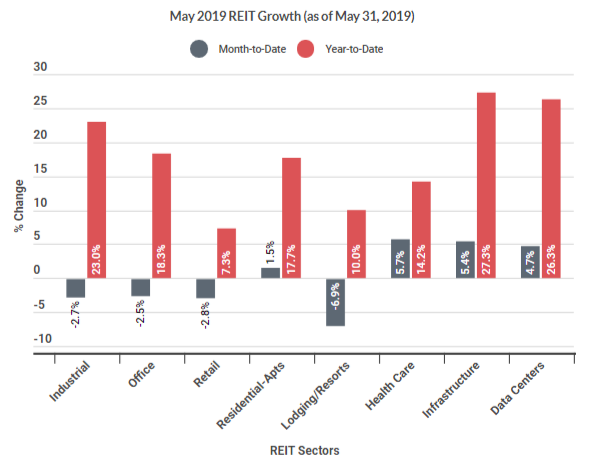

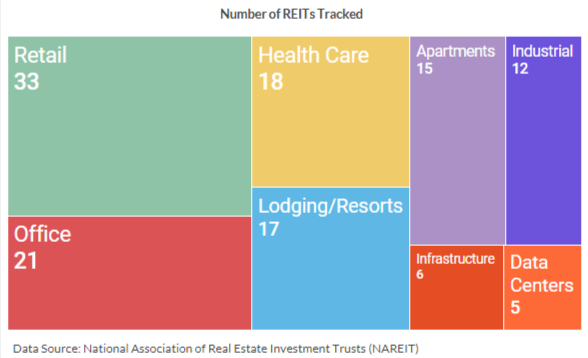

The sectors listed below, which were selected based on relevancy to Nevada, represent more than 75 percent of the 170 Financial Times Stock Exchange (FTSE) REITs currently being traded. It is useful to look at shorter-term and longer-term returns to determine trends.

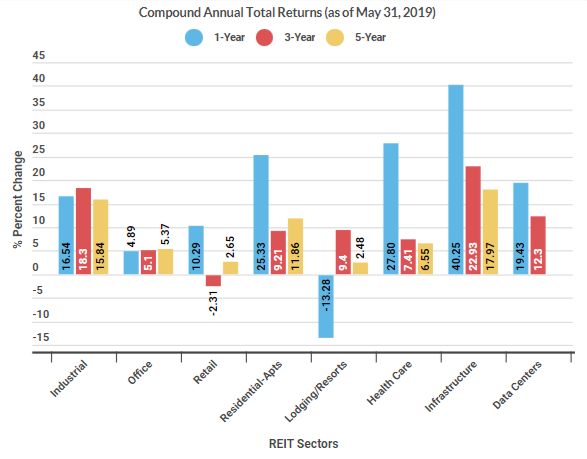

Overall, equity REITs, improved half a percentage point in May (versus April). The Healthcare sector rebounded by 10 percentage points with a monthly return of 5.73 percent, second only to Self-Storage (5.77 percent). Infrastructure and Data Centers also had another good month; Infrastructure now has the best one and three-year compound annual total returns (40.25 and 22.93 percent, respectively) of any sector NAREIT tracks. On a long-term basis, however, it has been the Manufactured Home sector of Residential that has the most impressive compound annual total returns: 22.91, 25.13, and 24.47 percent over three, five, and ten years, respectively.

A May 10, 2019 article in REIT Magazine sheds some light on the demand that is fueling the Manufactured Home sector. Baby-boomers who are downsizing, lower-income Americans, and working-class families with limited savings seek out manufactured home communities to enjoy the single-family home lifestyle and to escape rising rental prices of multifamily properties. REITs active in this sector include Equity LifeStyle Properties, Inc. (NYSE: ELS), Sun Communities, Inc. (NYSE: SUI), and UMH Properties Inc. (NYSE: UMH).

Though the Regional Mall sector has lost almost 2% over the past twelve months, some analysts are bullish on particular Mall REITs. The nation’s largest mall REIT, Simon Property Group (SPG), for example, has returned 4.67 percent over this period, beating the total returns for the S&P 500. A May 9, 2019 article in REIT Magazine attributes much of Simon’s success to redevelopment of existing properties: “Historically, redevelopment across the portfolio typically yields 6 to 10 percent, according to the company’s 10-K.” This redevelopment is the product of innovation; management is continually “testing and experimenting” with the shopping experience, including converting their malls into mixed-use destinations with entertainment, office space, hotels, and residential units.

As we described in our May newsletter, many analysts are bullish on the Industrial REIT sector, but a 2.7 percent loss in May and a May 28th article in Seeking Alpha remind us to pay attention to metrics other than annual total returns; metrics like Net Asset Value (NAV). Innovative Industrial Properties Inc. (NYSE: IIPR), for example, has been trading at a 139+ percent premium to its NAV. “[T]his premium to NAV may lead to superior growth” because of “access to cheap capital,” Jussi Askola writes, but “if the company disappoints in any way, it could quickly lead to sharp losses. When you command a 100% premium to NAV, you have much more to lose than when you trade at a reasonable 20% discount to NAV” and only have to . One is valued based on highly optimistic projections, whereas the other one only has toachieve minimal targets to satisfy the market.”