Welcome to our monthly REITView newsletter – where we analyze the latest national trends in real estate investment trusts (REITs) and their implications for investors and the Nevada real estate market. REITs own and often operate a pool of income-producing real estate assets. Investors can purchase a liquid stake in these portfolios – think of them as mutual funds for real estate.

While REITs are not the biggest players in Nevada’s commercial real estate landscape, secondary markets like Las Vegas with above-average population and job growth are likely to attract REITs looking for value and growth opportunities.

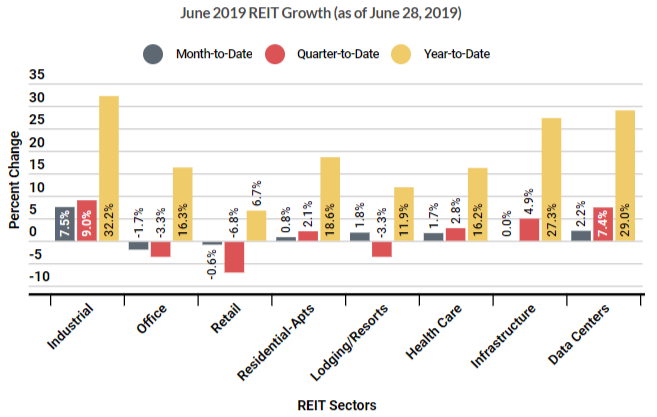

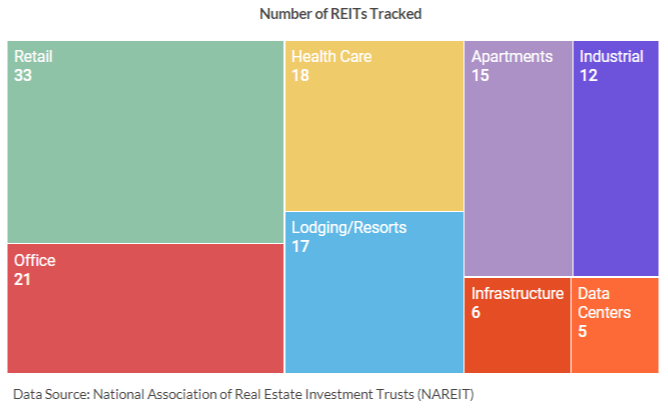

The sectors listed below, which were selected based on relevancy to Nevada, represent more than 75 percent of the 170 Financial Times Stock Exchange (FTSE) REITs currently being traded. It is useful to look at shorter-term and longer-term returns to determine trends.

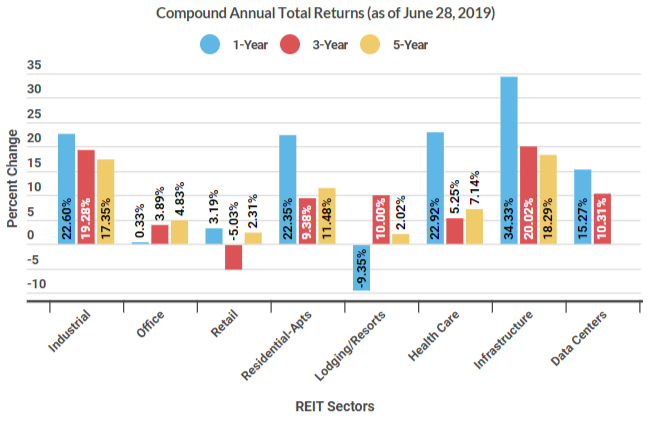

Overall, equity REITs gained three-quarters of a percentage point in June (versus May). After a disappointing May, the Industrial sector rebounded by 10 percentage points with a monthly return of 7.46 percent, followed by the Lodging/Resorts sector with an 8.69 percentage point rebound. The Industrial sector’s June performance was so strong, in fact, that it was a statistical outlier for the sectors that RCG tracks. On the wrong side of outliers, Regional Malls returned -12.63 percent for the quarter and -3.92 percent year-to-date. Infrastructure continues to have the best one and three-year compound annual total returns (34.33 and 20.02 percent, respectively), but its one-year return was weighed-down by a flat return in June. Industrial’s stellar month has boosted its three-year return to 19.28 percent. Manufactured Home REITS continue to have a considerable lead over the 5-year and 10-year horizons.

Given Industrial’s remarkable performance in June, let’s look at two REITs that were recently in the news. The Toby Awards are given annually by the Building Owners and Managers Association (BOMA) to recognize quality in commercial buildings and excellence in building management. Properties owned by Duke Realty Corp. (NYSE: DRE) and EastGroup Properties, Inc. (NYSE: EGP) were joint 2019 winners for the industrial office building category. Duke Realty’s nationwide portfolio of projects include state-of-the-art bulk warehouses and regional distribution centers, while EastGroup Properties focuses on ownership of premier distribution facilities in major Sunbelt markets generally clustered near major transportation features. EastGroup Properties’ one-year total return was 25.74 percent (as of July 15, 2019), exceeding the sector’s 22.6 percent total return.

As for Retail, over 7,000 store closures were announced by U.S. retailers in the first half of the year, according to tracking done by Coresight Research. “[T]he tally could top 12,000 by the end of 2019, setting a new record.” These closures are also bad news for U.S. mall owners like Simon and Macerich, which were already struggling with customer traffic. This is forcing landlords to get creative with their malls: more food options, e-commerce brands, offices, and even residential space (for more on mall REIT creativity, see our June issue of REITview).

Finally, from June 4th to June 6th NYC hosted the REITweek 2019 Investor Conference. The conference included a panel that discussed the state of capital markets, the likelihood of a near-term recession, and the impact of tariffs on REIT performance. Christy McElroy, senior equity research analyst at Citi, applauded the strong balance sheets that REITs have today, compared with historical averages, which should buffer them against the reality and possibility of further tariffs with China and Mexico. She also opined that self-driving cars and blockchain are poised to have a big impact on the REIT industry, ostensibly Infrastructure and Data Center REITs. The bad news according to the panel, however, is that some economists foresee a recession later this year that could impact the REIT market.

According to a July 11 article in Fortune, “Since the 1960s, one indicator of a looming recession has been the New York Fed’s recession probability index breaking 30%.” That prediction reached 32.9 percent in July—the highest probability since 2009. That said, the reader is advised to remember that this number also means that the New York Fed predicts a better than 77 percent chance that a recession will NOT occur in the near-term. There is always a recession up ahead–the economy moves in cycles; the question is, how long is the “near-term?”

For live charts, please visit https://infogram.com/july-reitview-1hnp27jpr0p82gq.