Welcome to our monthly REITView newsletter – where we analyze the latest national trends in real estate investment trusts (REITs) and their implications for investors and the Nevada real estate market. REITs own and often operate a pool of income-producing real estate assets. Investors can purchase a liquid stake in these portfolios – think of them as mutual funds for real estate.

While REITs are not the biggest players in Nevada’s commercial real estate landscape, secondary markets like Las Vegas with above-average population and job growth are likely to attract REITs looking for value and growth opportunities.

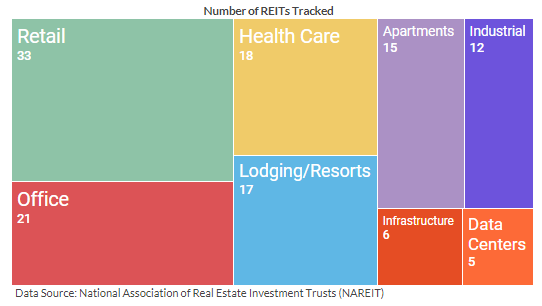

The sectors listed below, which were selected based on relevancy to Nevada, represent more than 75% of the 170 Financial Times Stock Exchange (FTSE) REITs currently being traded. It is useful to look at shorter-term and longer-term returns to determine trends.

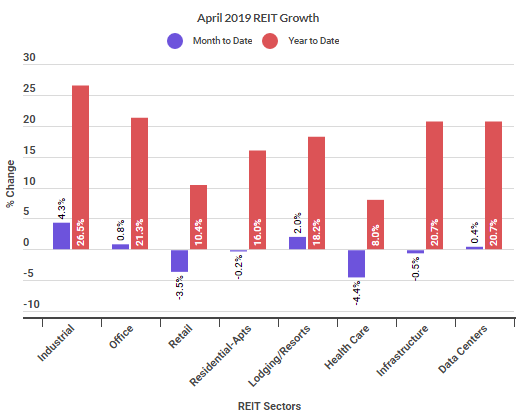

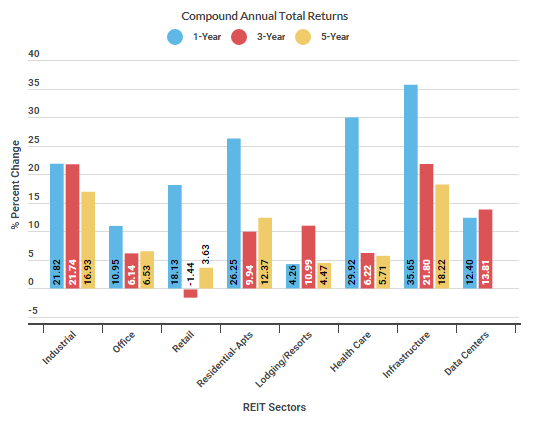

April saw a slight decline in return for equity REITs, weighed down by substantial declines in the Retail (especially malls) and Health Care sectors (-3.51 and -4.42 percent, respectively). The Industrial sector saw the strongest growth in April at 4.29 percent, but the biggest change versus March was in Lodging/Resorts, which improved 3.33 basis points from its March return. This sector has been erratic in 2019, posting growth of 4.2 percent in February, -1.3 percent for March, and 2.03 percent for April; Lodging/Resorts REITs are up 18.17 percent year-to-date, bolstered by the double-digit gains most REITs saw in January. The 12-month compound annual returns for most sectors are tremendously strong (up 19.56 percent for all equity REITs) except for Timber (down 21.4 percent) and the volatile Lodging/Resorts (up 4.26 percent).

The biggest movers versus March were the Infrastructure and Free Standing Retail sectors, though in the wrong direction–Infrastructure’s explosion in March retreated 11.14 basis points in April and Free Standing Retail is down 9.13 basis points from the previous month; but if you are long in those sectors, now is no time to panic.

Despite their April slowdown, Free Standing Retail and Infrastructure still lead the pack in 12-month compound total returns (40.34 and 35.65 percent, respectively), followed closely by Manufactured Homes (33.69 percent). Industrial and Infrastructure REITs continue strong growth over the past three years (21.74 and 21.80 percent, respectively), as do Manufactured Homes (23.7 percent).

The story remains the same for the five-year period, with Infrastructure (18.22 percent) and Industrial (16.93 percent) leading the way and Retail trailing at 3.63 percent. As discussed, some Retail categories have done quite well of late, however, and it appears that Free Standing Retail is taking significant market share from Regional Malls.

Analysts remain OPTIMISTIC FOR REITs THIS YEAR after a turbulent 2018. Rising interest rates and real estate taxes, in particular, took a toll on REIT performance last year. For 2019, RBC Capital Markets’ John Perkins likes REITs in the industrial, data center, and multifamily sectors, as does Tony Kenkel of Principal Global Real Estate Securities Fund. First quarter 2019 sales activity in The Valley’s industrial sector mirrors these analysts’ preferences–Cushman & Wakefield report that REIT buyers accounted for 44 percent of all industrial purchases in Q1 and showed a preference for large distribution centers. If you have a preference for the multifamily sector in The Valley, MAA owns two properties in North Las Vegas; the REIT focuses primarily on the acquisition, development, redevelopment and management of multifamily homes in the Southeast and Southwest.